The Build Back Better legislative package includes both taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. hikes and tax cuts, which contain two contrasting tax policy narratives. Tax hikes include corporate tax increases on foreign income and a new 15 percent domestic minimum tax, and green energy tax incentives provide a tax cut. Policymakers also sought to protect some pre-existing tax incentives from being negated by the domestic minimum tax and the Base Erosion and Anti-Abuse Tax (BEAT). However, the new global minimum tax casts doubt on the U.S. approach to tax incentives.

In the coming days, U.S. policymakers may have to choose between changing their approach to tax incentives or allowing U.S. companies to face higher tax bills in other countries. Whether or not Build Back Better passes, some tax benefits at home will just mean a tax increase abroad.

While U.S. legislators have aligned some pieces of Build Back Better to the global minimum tax (albeit with some remaining differences), the tax incentives that are baked into the U.S. tax code would create an opening for foreign jurisdictions to charge higher taxes on U.S. companies.

The global agreement sets a minimum effective tax rate of 15 percent that applies to multinational companies with revenues of more than €750 million (about U.S. $847 billion). Countries are not required to implement the rules, but the European Union has already begun their legislative process with a goal of applying the minimum tax by 2023. The global minimum tax has also been touted by Treasury Secretary Janet Yellen, who worked throughout 2021 to secure the agreement.

The minimum tax undermines tax incentives like tax holidays and tax credits in two ways. First, companies with foreign income that benefit from low taxes elsewhere will face a minimum effective tax rate of at least 15 percent imposed by “income inclusion rule.” Second, for multinational companies with domestic income that is taxed below 15 percent, foreign governments would be able to charge additional taxes through an “under-taxed payments rule.”

While policymakers are not required to change their tax incentives to comply with the global minimum tax, the value of those incentives will be directly eroded.

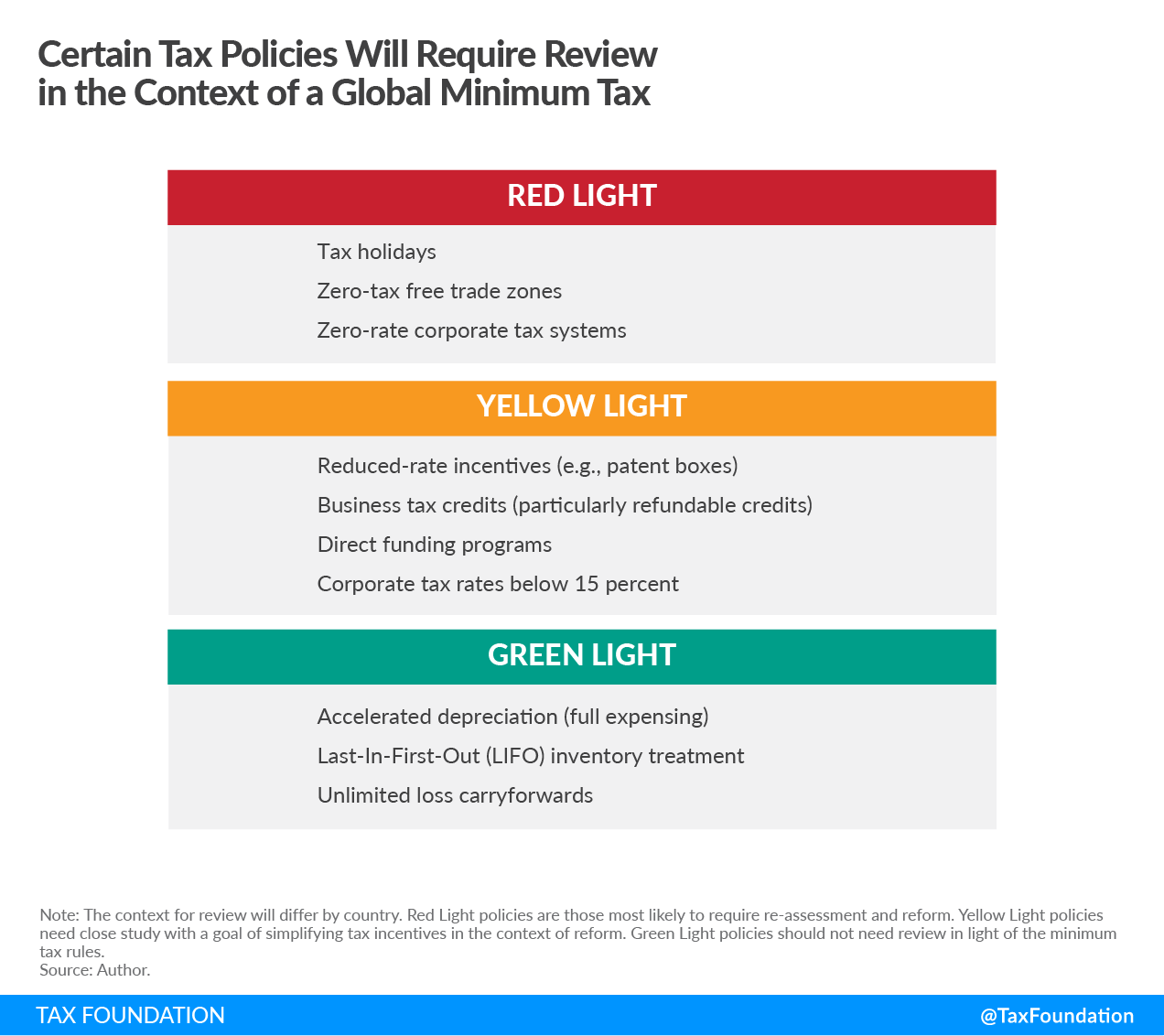

Recently, I outlined a framework for policymakers to consider in light of the global tax deal. Policies facing a “Red Light” are primarily those that provide a zero effective tax rate. “Yellow Light” policies provide reduced effective tax rates below 15 percent but not zero. “Green Light” policies are those that reduce the cost of investment while not triggering the minimum tax unless the general corporate tax rate is very low.

Many U.S. tax incentives sit in the “Yellow Light” zone. These policies include the Low-Income Housing Tax Credit, the Work Opportunity Tax Credit, preferences for green energy, and the Research & Development Tax Credit. The Foreign Derived Intangible Income policy, which provides a lower effective rate for exporters using intellectual property based in the U.S., also sits in the “Yellow Light” zone.

So, how do these incentives connect with the global minimum tax? Let’s say a U.S. company has operations in Japan and Germany, and both of those countries implement the global minimum tax. In the U.S., the company faces a 21 percent statutory tax rate on its profits, but it also benefits from the R&D credit and several other tax benefits related to its investment in climate friendly projects. These tax benefits could bring the effective tax rate on its U.S. profits down to 10 percent, below the global minimum rate of 15 percent.

The U.S. will tax foreign low-taxed profits of that company under the Global Intangible Low Tax Income (GILTI), the sort of U.S. version of an income inclusion rule. However, the domestic low-taxed profits could be targeted by Germany and Japan with the under-taxed payments rule.

Using a new formula in the model rules for the global minimum tax, Germany and Japan would share the ability to collect extra tax from the U.S. company based on their share of that company’s employees and assets. So even though the company would benefit from tax credits for R&D and green investment, thus reducing their tax bill to the U.S. Treasury, those benefits would be eaten up by higher taxes elsewhere. This removes the attractiveness of making those investments in the U.S.

This outcome can be true whether or not the Build Back Better passes and becomes law. To this point, lawmakers have specifically chosen to protect many tax credits from the impact of the 15 percent book minimum tax (a separate policy from the global minimum tax on foreign income) and from the BEAT.

Even when trying to raise revenue for other priorities in Build Back Better, members of Congress often care less about the fiscal cost of these policies than about influencing business investment behavior through tax incentives.

Tax incentives themselves are non-neutral policies and Congress could choose to do a thorough review and revamping of tax preferences in view of the global minimum tax. A tax code that is more neutral to business decisions would be much preferred (and less complex) than the current situation. If policymakers want to seize it, this provides an opportunity to broaden the corporate tax base and channel their efforts into general pro-growth reforms of the tax code.

Taxable grants and above-the-line credits would fare better under the global minimum tax than the way many U.S. tax credits are structured. Policymakers could choose to shift toward a tax incentive mix that includes those features.

On a narrower front, Sen. Ron Wyden (D-OR) has proposed a revamping of energy tax preferences. While Wyden’s proposal is imperfect, it goes a long way toward simplification. Even that package, though, could open large U.S. companies up to a tax cut at home that is offset by tax hikes abroad.

Focusing U.S. tax policy on simplicity and neutrality (alongside stability and transparency) will take a lot of work. But reforming the various tax incentives throughout the tax code would be valuable even if the global minimum tax was going to leave those credits alone.

Members of Congress could also engage in the ongoing work on the minimum tax rules. This work is not yet complete—especially because many governments have yet to begin the legislative process to implement the rules. The U.S. is not unique in having a variety of tax preferences that will be impacted by the global minimum tax, but it is unclear whether the U.S. Treasury appreciates the contrast between lawmaker’s approach in Build Back Better and the impact of the model rules on U.S. tax incentives.

Either way, the current prospect for the global minimum tax requires the attention of U.S. lawmakers. Otherwise, a tax benefit at home will just mean a tax increase abroad.